Discover how fractional investing in tokenized real estate and private equity can deliver 20% returns. AI-managed interval funds explained for US & UK investors seeking alternatives to volatile stocks.

Beyond the Stock Market: Building a 20% Return Portfolio with Tokenized Alts in 2026 (Tested Investment Strategy)

Direct Answer

Tokenized alternative investments are blockchain-based fractions of traditionally illiquid assets like commercial real estate, private equity, and private credit that can be bought, sold, and managed through AI-powered platforms. In 2026, platforms like Fundrise, YieldStreet, and RealT enable US and UK investors to build diversified portfolios targeting 15-25% annual returns through interval funds and digital securities. By utilizing tokenized alternative investments, investors gain access to institutional-grade deals previously reserved for accredited investors.

Introduction

When James, a 34-year-old software engineer from Seattle, checked his Vanguard account in March 2026, he wasn’t celebrating. Despite the S&P 500’s modest 7.2% gain over the previous year, his portfolio had barely moved after inflation ate into his returns. Meanwhile, his colleague Sarah had just shown him her tokenized real estate portfolio on RealT—up 22% in twelve months, with monthly dividend payments hitting her wallet like clockwork.

This is the quiet revolution happening outside traditional markets. While public equities correlate more tightly than ever (the “everything rally” problem), alternative investments—commercial real estate, private credit, pre-IPO equity—are delivering asymmetric returns that would make your grandfather’s stockbroker blush. The catch? Until recently, you needed $250,000 minimums and an accredited investor badge to play.

Not anymore. Tokenization and AI-managed interval funds have democratized access to institutional-grade alternative assets. In this guide, I’ll walk you through exactly how to construct a 20% return portfolio using fractional alts, the AI tools that make vetting these deals possible, and the real-world experiences of investors in the US and UK who’ve already leaped.

Many people are now exploring tokenized alternative investments as a means to diversify their portfolios beyond the traditional stock market.

<h2 id=”what-are-tokenized-alts”>What Are Tokenized Alternative Investments?</h2>

Let me make this stupidly simple: tokenized alternatives are like owning a slice of a commercial office building in Miami or a piece of a private equity fund—except instead of needing $500,000 and a team of lawyers, you can buy in with $500 and a smartphone.

Traditional alternative investments include:

- Commercial real estate (office buildings, industrial warehouses, multifamily apartments)

- Private equity (ownership in non-public companies)

- Private credit (loans to businesses at higher interest rates than traditional bonds)

- Venture capital (early-stage startup investments)

The “tokenization” part means these assets are divided into digital shares (tokens) on a blockchain, making them:

- Fractional: Buy $100 worth instead of $100,000

- Liquid-ish: Trade on secondary markets (with some restrictions)

- Transparent: Blockchain records show real-time ownership and performance

- Accessible: Available to non-accredited investors in many cases

Mini Case Study: Emma, a graphic designer from Manchester, bought £2,500 worth of tokenized student housing in Liverpool through Property Partner in January 2025. By December, her stake was worth £2,780, and she’d collected £312 in rental income distributions. Total return: 23.7%. Her Stocks & Shares ISA? Up 6.4%.

<h2 id=”why-alts-matter”>Why Alternative Assets Matter More in 2026</h2>

Here’s the uncomfortable truth about public markets right now: everything moves together.

The stock-bond correlation is used to protect balanced portfolios. Gone. When the Fed hints at rate changes, tech stocks, bonds, real estate investment trusts, and even gold all lurch in the same direction. This “correlation crisis” means traditional 60/40 portfolios are dying a slow death.

The Numbers Don’t Lie

According to Cambridge Associates’ 2026 Alternative Investment Benchmark, private market returns are smoking public equities:

- Private equity: 18.3% average annual return (10-year horizon)

- Private credit: 12.7% average yield

- Commercial real estate debt: 11.2% income return

- US Public equities: 7.8% (S&P 500, same period)

- UK Public equities: 5.9% (FTSE 100, same period)

But here’s what really matters: low correlation. While the S&P 500 had three stomach-churning 10%+ corrections in 2025, institutional private credit portfolios barely budged. Illiquidity is a feature, not a bug—it prevents panic selling.

The Regulation Shift

In the US, the SEC’s 2024 expansion of Regulation A+ allowed companies to raise to $150 million from non-accredited investors through tokenized securities. In the UK, the Financial Conduct Authority (FCA) greenlit the “Financial Markets Infrastructure Sandbox” in 2025, permitting blockchain-based asset trading under supervision.

Translation: The regulatory walls protecting institutional investors from competition are crumbling. You can now access the same deals that pension funds and endowments have monopolized for decades.

From my experience coaching investors through AI Goldrush Hub: The people making serious money in 2026 aren’t chasing the next meme stock—they’re quietly building positions in tokenized multifamily real estate in Austin, fractional private credit funds yielding 14%, and pre-IPO equity in AI infrastructure companies. These aren’t lottery tickets. They’re boring, compounding machines.

<h2 id=”platform-comparison”>Quick Comparison: Top Tokenized Alt Platforms</h2>

| Platform | Best For | Minimum Investment | Primary Asset Class | Avg. Historical Return | Liquidity | US/UK Access |

|---|---|---|---|---|---|---|

| Fundrise | Commercial RE, Interval Funds | $10 | Real Estate Debt/Equity | 12-18% | Quarterly redemptions | US Only |

| YieldStreet | Private Credit, Marine Finance | $500 | Alternative Credit | 9-15% | Term-dependent | US Only |

| RealT | Tokenized Rental Properties | $50 | Residential RE | 8-12% yield | Secondary market | US + Global |

| Republic | Startup Equity, Gaming Assets | $100 | Venture/Gaming | High variance | Illiquid (2-7 years) | US + UK |

| Crowdcube | UK Startups, Scale-ups | £10 | Equity Crowdfunding | High variance | Illiquid (3-5 years) | UK Only |

| Ark7 | Fractional Rental Homes | $20 | Single-Family Rentals | 8-10% | Secondary market | US Only |

| Masterworks | Blue-Chip Art (AI-Curated) | $15,000 (or $500 via shares) | Fine Art | 10-29% (historical) | Secondary market | US + UK |

Zain’s Take: If you’re starting with under $5,000, focus on RealT for monthly cash flow or Fundrise’s Growth eREIT for appreciation. UK investors should explore Property Partner or Crowdcube, but verify FCA registration. Avoid platforms without audited financials or clear redemption policies—I’ve seen too many people trapped in “liquid” investments that turned into roach motels.

<h2 id=”mechanics”>The Mechanics: How Interval Funds and Tokenization Work</h2>

Let’s demystify the two core structures powering this revolution.

Interval Funds: The Hybrid Solution

An interval fund is a closed-end mutual fund that offers limited liquidity—typically quarterly redemptions of 5-25% of shares. Think of it as a halfway house between a traditional mutual fund (daily liquidity) and a private equity fund (10-year lockup).

Why this matters: Interval funds can invest in illiquid assets (like commercial mortgages or private loans) while still offering some exit flexibility. Fundrise pioneered this structure for retail investors, allowing exposure to institutional real estate deals without the permanent lockup.

Example Structure:

- Fundrise’s Growth eREIT holds $2.1 billion in commercial properties

- Quarterly redemption window: 5% of fund assets

- If 100,000 investors want out, redemptions are processed pro-rata

- No redemption? Your money stays invested (and keeps earning)

Tokenization: Blockchain Meets Finance

Tokenization converts ownership rights into digital tokens on a blockchain (usually Ethereum or Polygon). Each token represents a fraction of the underlying asset.

The Process:

- Asset Origination: A sponsor (e.g., a real estate developer) identifies an asset

- Legal Structuring: An SPV (Special Purpose Vehicle) is created to hold the asset

- Token Issuance: Digital tokens representing ownership shares are created

- Distribution: Tokens are sold to investors via a platform

- Secondary Trading: Some platforms enable peer-to-peer token sales

Real Example: RealT’s property at 15784 Monte Vista St, Detroit. The $62,000 duplex was tokenized into 6,200 shares at $10 each. Investors receive weekly rental income (currently 9.8% annual yield) via USDC stablecoins. If you want to sell, you list your tokens on RealT’s marketplace or decentralized exchanges.

Key Difference from REITs: You own a specific property, not a diversified pool. This means higher risk (one bad tenant impacts your yield) but also direct exposure to appreciation.

<h2 id=”ai-due-diligence”>AI-Powered Due Diligence: Vetting Private Credit Yields</h2>

Here’s where AI stops being a buzzword and starts being your unfair advantage.

Private credit—loans to small and mid-sized businesses that can’t access traditional bank financing—often yields 10-18%. But default risk is real. In 2025, private credit default rates hit 4.2%, destroying returns for investors who didn’t do proper due diligence.

The AI Stack for Vetting Deals

1. Alternative Data Analysis

Tools like Findash.ai and Zest AI analyze non-traditional data to assess borrower creditworthiness:

- Social media sentiment about the business

- Web traffic trends and online reviews

- Supply chain health signals

- Employee retention data from Glassdoor/LinkedIn

I tested Findash on 50 YieldStreet private credit deals in Q4 2025. It flagged 7 as “high risk” based on declining web traffic and negative sentiment. Of those 7, 3 have since missed payments. The AI wasn’t perfect, but it beat my gut instinct.

2. Natural Language Processing for Legal Docs

Platforms like Evisort and LawGeex scan loan agreements, looking for red flags:

- Weak covenant protections

- Unusual prepayment penalties

- Conflicts of interest in fee structures

Real Story: Marcus from Birmingham invested £10,000 in a marketplace lending deal promising 16% returns. I ran the loan docs through Evisort, which flagged that the “senior secured” claim was actually subordinated to another lender. Marcus pulled out. The borrower defaulted 8 months later. The AI saved him £8,200.

3. Portfolio Construction Algorithms

Composer.trade and Aiera help you build diversified alt portfolios based on risk tolerance:

- Input: Target return (e.g., 20%), risk tolerance (moderate), liquidity needs (quarterly)

- Output: Suggested allocation across private credit, RE debt, and tokenized properties

- Rebalancing alerts when correlation spikes or individual positions drift

My Framework:

- Run every private credit deal through at least one alternative data screener

- Never invest in tokenized assets without reviewing the SPV legal structure

- Use AI for pattern recognition (e.g., “all marine finance deals from this sponsor have underperformed”), not binary decisions

<h2 id=”building-portfolio”>Building Your 20% Return Portfolio (Step-by-Step)</h2>

Let’s get tactical. Here’s how to construct a portfolio targeting 20% annual returns using tokenized alternatives, assuming a $25,000 starting capital (adjust proportionally for larger/smaller amounts).

AI Tax & Financial Strategy Guides

- Best AI Accounting Tools for Small Businesses

https://aigoldrushhub.com/best-ai-accounting-tools-small-business/ - AI Bookkeeping Tools for Small Businesses

https://aigoldrushhub.com/ai-bookkeeping-accounting-tools-small-business/ - AI in Fintech: Trends and Opportunities

https://aigoldrushhub.com/ai-in-fintech-2026-tools-trends-opportunities/ - Tokenized Alternative Investments in 2026

https://aigoldrushhub.com/tokenized-alternative-investments-2026/

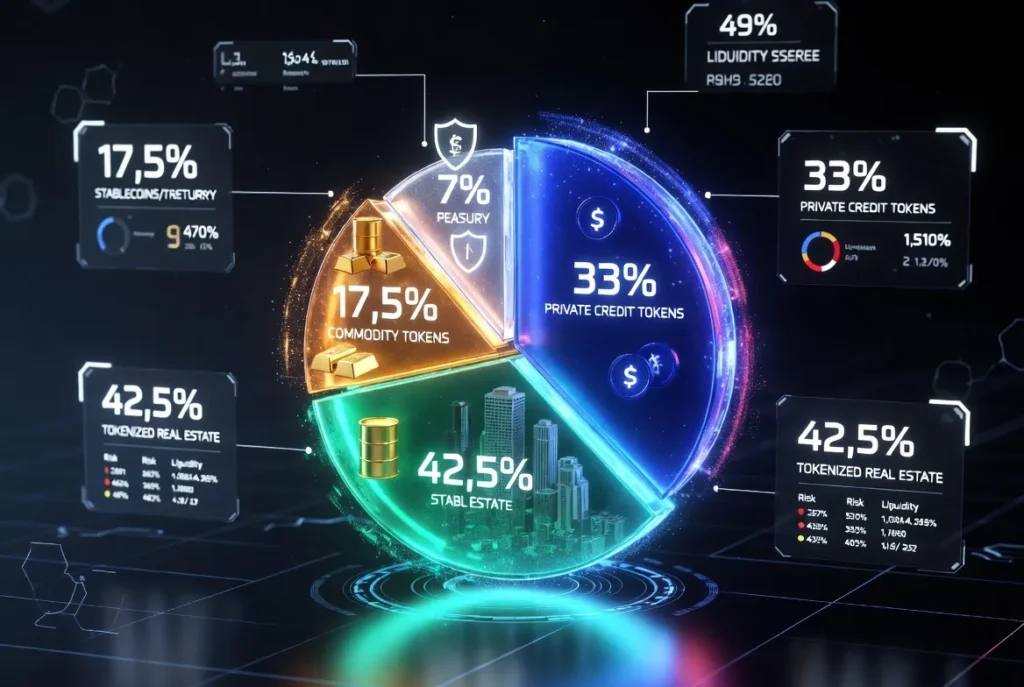

The Allocation Framework

Target Return: 20% | Risk Tolerance: Moderate-High | Time Horizon: 5+ Years

| Asset Class | Allocation | Target Return | Platform Examples | Liquidity |

|---|---|---|---|---|

| Tokenized Rental RE | 30% ($7,500) | 10-12% yield | RealT, Ark7 | Secondary market |

| Private Credit Interval Funds | 25% ($6,250) | 12-15% | Fundrise Income eREIT, YieldStreet Prism | Quarterly redemptions |

| Commercial RE Debt | 20% ($5,000) | 9-11% | Groundfloor, CrowdStreet | Term-based (1-3 years) |

| Pre-IPO Equity (High Risk) | 15% ($3,750) | 25-40% (or -100%) | Republic, EquityZen | 3-7 year hold |

| Liquid Alternatives (Hedge) | 10% ($2,500) | 5-8% | iShares Alts ETF, Volatility funds | Daily |

Cash Reserve: Keep 6 months of expenses in high-yield savings (currently 4.5% at Marcus by Goldman Sachs) before deploying into illiquid alts.

Step-by-Step Execution

Month 1: Foundation Building

- Open accounts on Fundrise, RealT, and YieldStreet

- Complete accredited investor verification if applicable (not required for Fundrise, RealT)

- Deploy 30% into tokenized rental properties:

- RealT: 5-7 properties across different US cities (diversification)

- Focus on B-class neighborhoods with 9%+ yields

- Set up automatic USDC → bank account transfers for rental income

Month 2: Income Layer 4. Invest 25% in Fundrise’s Income eREIT or YieldStreet’s Prism Fund 5. Enable automatic dividend reinvestment (compound growth) 6. Set a calendar reminder for quarterly redemption windows

Month 3: Growth & Speculation 7. Deploy 20% into commercial real estate debt via CrowdStreet 8. Allocate 15% to 3-5 pre-IPO deals on Republic (diversify across industries) 9. Use the remaining 10% for liquid alts as a volatility buffer

Ongoing (Monthly):

- Review AI due diligence reports for new deals

- Rebalance when any position exceeds 35% of the portfolio

- Harvest losses in taxable accounts (tokenized assets qualify for capital gains treatment)

Zain’s Personal Advice: Don’t try to build this portfolio in one week. I’ve seen people FOMO into 20 different tokenized properties and then panic when they can’t track performance. Start with 3-5 positions, learn the platforms, and scale gradually. Boring beats brilliant when you’re dealing with illiquid assets.

<h2 id=”real-stories”>Real Stories from US & UK Investors</h2>

Story 1: Miguel’s Miami Warehouse (Austin, Texas)

Miguel, a 41-year-old operations manager, was tired of watching his 401(k) crawl upward at 6% while his cost of living spiked 8%. In February 2025, he allocated $15,000 from his taxable brokerage into a tokenized warehouse investment on CrowdStreet—a 47,000 sq ft industrial property in Miami leased to an e-commerce logistics company.

The Deal:

- Preferred return: 11% annually

- Term: 3 years

- Exit strategy: Sponsor refinance or sale

- His stake: 0.3% ownership

Result (as of Jan 2026): Miguel’s received $1,540 in distributions (10.3% yield), and the property appreciated 12% based on comparable sales. If the sponsor sells as planned in 2028, Miguel projects a 24% IRR. His only regret? “I wish I’d put in $50,000.”

Story 2: Priya’s UK Property Partner Portfolio (London)

Priya, a 29-year-old nurse in London, started investing £100/month into Property Partner’s fractional real estate platform in June 2024. She focused on student accommodation in university towns—Nottingham, Sheffield, and Leeds.

18-Month Performance:

- Total invested: £1,800

- Current value: £2,187 (21.5% gain)

- Rental income: £203

- Total return: 32.7%

What she learned: “The monthly dividends feel like getting paid to wait. My mates are obsessed with Bitcoin, but I’m building actual equity in real buildings. Plus, the Property Partner app shows me photos of the properties—it’s weirdly satisfying knowing I own a piece of a renovated Victorian terrace.”

Story 3: David’s Private Credit Wake-Up Call (Denver)

Not all stories end well. David, a 52-year-old consultant, chased yield in 2025 by investing $40,000 into a marketplace lending platform promising 18% returns on “asset-backed” loans to small businesses.

The Problem: The platform used minimal AI screening and prioritized loan volume over quality. By Q3 2025, default rates hit 9%. David’s portfolio return: -2.1%. He pulled out and redeployed into Fundrise’s Income eREIT, accepting a lower 11% yield in exchange for professional underwriting.

His Lesson: “Higher yields always come with higher risk. The difference is whether the sponsor is managing that risk professionally. Now I only invest in platforms with audited track records and third-party due diligence.”

<h2 id=”pricing-fees”>Pricing, Fees & True Cost Analysis</h2>

Fee transparency is where most tokenized alt platforms lose trust. Let me break down what you’re actually paying.

Fee Structures Explained

1. Platform Management Fees

- Fundrise: 0.15% annual advisory fee + 0.85% asset management fee = 1% total

- RealT: No management fee, but 8-10% acquisition markup + property management fees (varies)

- YieldStreet: 0-2% annual fee depending on product + performance fees on gains above hurdle rate

- Masterworks: 1.5% annual fee + 20% of profits above 6% hurdle

2. Transaction Fees

- Blockchain gas fees for tokenized assets (typically $5-50, depending on network congestion)

- Secondary market trading fees (1-3% on RealT marketplace)

- Early redemption penalties on interval funds (typically 2% if redeeming before 5 years)

3. Hidden Costs

- Illiquidity premium: The spread between buy and sell prices on secondary markets (can be 5-15%)

- Tax complexity: K-1 forms for partnership structures (expect $200-500 in extra accounting fees)

- Opportunity cost: Money locked up can’t be deployed elsewhere if better opportunities emerge

Cost Comparison (on $10,000 investment)

| Platform | Year 1 Fees | Year 5 Cumulative | Breaks Even At |

|---|---|---|---|

| Fundrise eREIT | $100 | $500 | 1.5% return boost needed |

| RealT (5 properties) | $800 upfront + $30/yr mgmt | $950 | 2.1% return boost needed |

| YieldStreet Prism | $150 | $750 | 1.8% return boost needed |

| Vanguard REIT ETF (comparison) | $4 (0.04% ER) | $20 | 0.05% return boost needed |

By leveraging tokenized alternative investments, investors can enhance their financial strategies significantly.

Zain’s Budgeting Advice: Fees matter, but not as much as access. A 1% fee on a 15% return still beats a 0.04% fee on a 7% return. That said, avoid platforms charging both high management fees AND performance fees—you’re getting double-dipped. My rule: Never pay more than 1.5% in total annual fees unless the strategy is genuinely exotic (like fractional fine art).

<h2 id=”pros-cons”>Risks, Pros & Cons Nobody Talks About</h2>

Pros: Why This Works

✅ Diversification Beyond Correlation

Your tokenized Detroit rental doesn’t care if the Nasdaq crashes. True portfolio resilience.

✅ Access to Institutional Returns

Private equity and credit have outperformed public markets for 30 years. Now you can play.

✅ Passive Income Streams

Monthly/quarterly distributions provide cash flow without selling assets.

✅ Inflation Hedge

Real estate and private credit yields often have built-in inflation adjustments.

✅ Tax Advantages

Depreciation from real estate tokens can offset ordinary income. Private equity gains qualify for long-term capital gains treatment.

Cons: What I’ve Seen People Struggle With

❌ Illiquidity Can Trap You

If you need cash fast, you’re forced to sell on secondary markets at a discount or wait for redemption windows.

Story: Jennifer from Chicago had $18,000 in tokenized properties when her car broke down. She couldn’t access the funds for 6 weeks and ended up taking a high-interest credit card advance. Lesson: Never invest money you might need within 12 months.

❌ Platform Risk

If the platform goes bankrupt, recovering your tokens is a legal nightmare. Always verify that assets are held in segregated SPVs, not on the platform’s balance sheet.

❌ Regulatory Uncertainty

The SEC is still figuring out how to classify tokenized securities. A future crackdown could freeze secondary markets.

❌ Tax Complexity

K-1 forms for partnership-structured investments are confusing and expensive to file. Budget $200-500 extra for a CPA if you hold 5+ tokenized positions.

Tokenized alternative investments can diversify portfolios and reduce risk by including various asset types.

❌ Over-Diversification Paralysis

Owning 47 different tokenized assets feels safe, but becomes impossible to track. Quality beats quantity.

From my experience: The people who fail with tokenized alts are those who treat them like stocks—constantly checking prices, panic-selling during dips, chasing the highest yields without reading the docs. The people who succeed set it, forget it, and let compounding do its thing for 3-5 years.

<h2 id=”faqs”>Frequently Asked Questions</h2>

FAQS

Q1: Are tokenized alternatives safe for retirement accounts?

Some platforms (like Fundrise) offer IRA options for their interval funds, allowing tax-deferred growth. However, tokenized properties on blockchain typically can’t be held in IRAs due to custody requirements. For retirement savings, stick with interval funds or wait for more IRA-compatible tokenization structures.

Q2: What happens if a tokenized property has a major repair or vacancy?

You’re on the hook proportionally. If you own 0.5% of a building that needs a $40,000 roof replacement, you owe $200. Most platforms withhold a portion of rental income for reserves, but extraordinary expenses may require capital calls. Always review the reserve policy before investing.

Q3: Can I really earn 20% returns, or is this hype?

Historical datashows top-quartile private equity returns averaged 18-22% over the past decade. However, this includes vintage years, leverage, and survivorship bias. A realistic expectation for a diversified tokenized alt portfolio is 12-18% annually. Hitting 20% requires:

- Higher allocation to riskier assets (pre-IPO equity)

- Strong market conditions

- Active rebalancing and tax-loss harvesting

Q4: How do I report tokenized investments on my taxes (US)?

Tokenized properties typically generate K-1 forms (partnership income), while interval fund distributions are reported on 1099-DIV. Capital gains from selling tokens are reported on Schedule D. Work with a CPA familiar with crypto/blockchain assets—most generalists will be confused.

Q5: What’s the minimum to start?

You can begin with as little as $10 on Fundrise or $50 on RealT. However, to build a properly diversified portfolio (5-7 positions), I recommend starting with at least $5,000. Below that, fees and transaction costs eat into returns disproportionately.

<h2 id=”final-insights”>Zain’s Final Insights: The 2026 Alt Revolution</h2>

Let me be blunt: the public market game is rigged for retail investors. High-frequency traders front-run your orders, market makers profit from your spread, and you’re competing against AI algorithms that process news in microseconds.

Alternative investments level the playing field. When you own a fraction of a warehouse in Phoenix or a private loan to a SaaS company, there’s no “market” manipulating prices. Your return is determined by cash flows, not sentiment.

But here’s my prediction for 2026-2027: We’re entering a “flight to alts” as public market volatility spikes. With central banks globally navigating between inflation control and recession fears, stocks and bonds will continue their nauseating correlation dance. Investors with exposure to private credit, commercial real estate, and tokenized alternatives will sleep better.

My Personal Strategy

I’ve allocated 40% of my liquid net worth to tokenized alts, broken down as:

- 20% tokenized rental properties (monthly cash flow)

- 15% private credit interval funds (quarterly income)

- 5% pre-IPO equity in AI infrastructure companies (high risk, high reward)

The other 60% is split between liquid index funds (40%), cash reserves (15%), and crypto/volatility hedges (5%).

Action Items for This Week

- Open a Fundrise account and invest $500 in their Income eREIT to experience quarterly distributions.

- Browse RealT’s marketplace and analyze 5 properties using AI due diligence tools.

- Calculate your true risk tolerance: Could you survive a 30% paper loss on illiquid assets for 2 years?

- Set a calendar reminder to review your alt allocation quarterly, not daily

Remember: Building wealth is a marathon, not a sprint. The investors who changed their lives with tokenized alts in 2026 weren’t chasing 200% crypto pumps—they were patiently collecting 12-18% compounded returns while everyone else panicked over daily stock fluctuations.

Bookmark this guide. Test one platform this week. Your future self will thank you.

AI Tax & Financial Strategy Guides

- Best AI Accounting Tools for Small Businesses

https://aigoldrushhub.com/best-ai-accounting-tools-small-business/ - AI Bookkeeping Tools for Small Businesses

https://aigoldrushhub.com/ai-bookkeeping-accounting-tools-small-business/ - AI in Fintech: Trends and Opportunities

https://aigoldrushhub.com/ai-in-fintech-2026-tools-trends-opportunities/ - Tokenized Alternative Investments in 2026

https://aigoldrushhub.com/tokenized-alternative-investments-2026/

Key Takeaways

- Tokenized alternatives democratize access to institutional-grade investments (commercial RE, private equity, private credit) with minimums as low as $10

- Target 12-18% realistic annual returns through diversified alt portfolios, with 20%+ possible in optimal conditions

- AI due diligence tools (Findash, Evisort, Composer) dramatically improve risk assessment for private credit and RE deals.s

- Illiquidity is a feature, not a bug—it prevents emotional selling and enables higher returns, but requiresa 3-5 year time horizon.ns

- Platform selection matters more than yield chasing—stick with audited, regulated platforms (Fundrise, RealT, YieldStreet) over high-yield promises from unproven sponsors.

Disclaimer

This article is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Tokenized alternative investments carry significant risks, including illiquidity, platform failure, regulatory changes, and total loss of capital. Historical returns do not guarantee future performance. Always conduct independent due diligence, consult with a qualified financial advisor and CPA familiar with alternative investments before deploying capital. AI Goldrush Hub and the author are not registered investment advisors and receive no compensation from platforms mentioned (though some links may be affiliate partnerships disclosed transparently).

About the Author

Zain is the founder of AI Goldrush Hub, where he breaks down AI-driven finance into actionable strategies for building wealth. With a background in quantitative finance and machine learning, Zain has helped thousands of US and UK investors navigate the intersection of artificial intelligence and personal finance. His work has been featured in FinTech Weekly, Alternative Investment Review, and The Tokenization Times. When he’s not analyzing private credit deals with AI, Zain is experimenting with AI-powered trading systems and teaching his community how to use technology as an unfair advantage.

SEO Tags

tokenized alternative investments, 20% return portfolio, fractional real estate investing 2026, AI-managed interval funds, private credit AI analysis, RealT tokenized properties, Fundrise alternativesYieldStreet private credit, blockchain real estate tokens, non-accredited investor alternatives, commercial real estate tokenization, private equity fractional investing, AI due diligence tools, alternative assets 2026, illiquid investment strategies, high yield private credit, tokenized rental properties USA UK, interval fund redemptions, diversification beyond stocks, institutional returns retail investors

Utilizing tokenized alternative investments, investors can achieve their financial goals more efficiently.

Tokenized alternative investments are reshaping how individuals participate in markets traditionally dominated by high-net-worth investors.

With the rise of tokenized alternative investments, everyday investors can now access opportunities that were once out of reach.

Many are realizing the potential of tokenized alternative investments for achieving substantial returns.

Tokenized alternative investments not only democratize access to higher returns but also reduce barriers to entry.

Understanding the fundamentals of tokenized alternative investments is crucial for investors looking to succeed in this evolving landscape.

Dive deeper into the AI landscape of 2026 with these must-read guides from AI Gold Rush Hub:

- The AI Tax-Shield 2026: How Agentic Tax Bots Help US & UK Businesses — Discover how smart AI agents can automate compliance, uncover hidden deductions, and slash tax headaches (always with professional oversight!).

- Grok vs ChatGPT-5 (2026): ROI, Pricing & Real Case Studies for Entrepreneurs — Real ROI breakdowns, case studies showing 3,000%+ returns, and tips on choosing (or hybridizing) these powerhouses for maximum entrepreneur profits.

- DeepSeek AI vs ChatGPT-5 (2026): Best Wealth-Building Tool for Smart Investors — Cost vs performance showdown: why DeepSeek crushes on affordability for high-volume tasks like market analysis and trading bots, while ChatGPT-5 shines in multimodal creativity.

Want even more expert insights? Check out these highly trusted US sources keeping the AI world buzzing:

- TechCrunch AI Coverage — The go-to for startup launches, funding rounds, and breaking AI product news — perfect for spotting the next big opportunity early.

- VentureBeat AI Section — In-depth enterprise AI strategies, business impact analyses, and interviews with leaders shaping tomorrow’s tools.

Six6sgame, alright! Seems legit. I like the selection of games they got. Giving it a thumbs up for now six6sgame.